Article

Recommendation 1: We recommend that additional resourcing and specialized training be provided to law enforcement and the courts to be able to effectively address and stop the occurrence of scams that are being generated at an accelerated rate, to protect Albertans.

Recommendation 2: Given the importance of interoperability and harmonization to consumers and businesses, we recommend the Government of Alberta continue to align its Personal Information Protection Act (PIPA) to the principles-based approach of federal privacy legislation as it will facilitate a consistent approach to private sector privacy domestically and globally for Alberta businesses and Albertans, who will benefit from a consistent approach to understanding their rights in relation to their personal information. We also recommend any new or amended definitions in PIPA be harmonized with existing private sector definitions and concepts, as inconsistent privacy requirements for the private sector may lead to increased compliance costs and obstacles to innovation. Lastly, any reform efforts should support pending or future federal initiatives aimed at increasing protections (e.g., combatting financial crime) or encouraging innovation (e.g., Consumer-Driven Banking).

Recommendation 3: We urge the Government of Alberta to work closely with the federal government and authorities to combat money laundering (ML) and terrorist financing (TF). In particular, we urge investments in Alberta’s enforcement and prosecution of ML and TF and the harmonization of its existing tools with the federal government. A harmonized approach will ensure efficiency by avoiding compliance duplication across different levels of government.

Recommendation 4: We encourage the Government of Alberta to support the adoption of a financial consumer protection regime targeted at payment service providers (PSPs), as part of Alberta’s consumer protection framework. Enhancing standards for financial consumer protection should also extend to entities that embed payments processing for merchants on behalf of consumers that have the potential to fall outside the federal framework, as they introduce the same risks as PSPs. We also encourage Alberta to work with other provinces and the federal government to achieve a consistent market conduct framework across the country for the benefit of consumers and PSPs.

Recommendation 5: We urge the Government of Alberta to provide policy and regulatory support to provincially regulated credit unions that want to transition to the federal credit union framework, increase transparency in the provincial credit union system, and realign credit unions’ unlimited deposit guarantees to international and national best practices.

Recommendation 6: We recommend implementing innovative, aggressive, and comprehensive solutions to address public safety and security challenges that impact community vitality and economic growth. Urgent and additional funding is required to enhance community vibrancy projects, expand pre-and post-addiction recovery services and support enhanced mobile crises response units. Additional efforts should be made to expand the adoption of digital payment options for all social benefits recipients.

Recommendation 7: We recommend the Government of Alberta continue to undertake productivity-enhancing tax reforms in the province and advocate at the federal level for a comprehensive review of our country’s tax system. Canada must modernize its tax system and avoid asymmetrical, sector-specific taxes, and retroactive tax legislation that ultimately impacts businesses and consumers as well as undermines certainty around investment decisions.

Introduction

The CBA is grateful for the opportunity to contribute to the Government of Alberta’s upcoming budget. As the voice of more than 60 domestic and foreign banks, we advocate for public policies that contribute to a sound and safe banking system that helps drive prosperity for Canadians and economic growth for Canada.

Banking Sector’s Economic Contributions

Banks play an important role in Alberta’s economy. In 2023, banks1:

- Contributed over $8.8 billion (or 2.6%) to Alberta’s GDP.

- Paid approximately $200 million in taxes.

- Employed close to 18,900 people, a workforce represented by women (62%) and self-identified visible minorities (41%).

- Generated over $28 billion in dividend income that went to Canadian (including Albertan) seniors, families, pensions, charities, and endowments.

- Banks operated close to 740 branches and over 2,400 ABMs in the province.

Banks are key in providing access to capital for Albertans. By the end of 2023, they had:

- Over $165 billion in residential mortgages outstanding.

- Over $238 billion in authorized business credit, of which $32.1 billion went to support small- and medium-sized enterprises (SMEs).

- Since 2010, small business debt approval rates in the province have consistently been above 78% annually.2

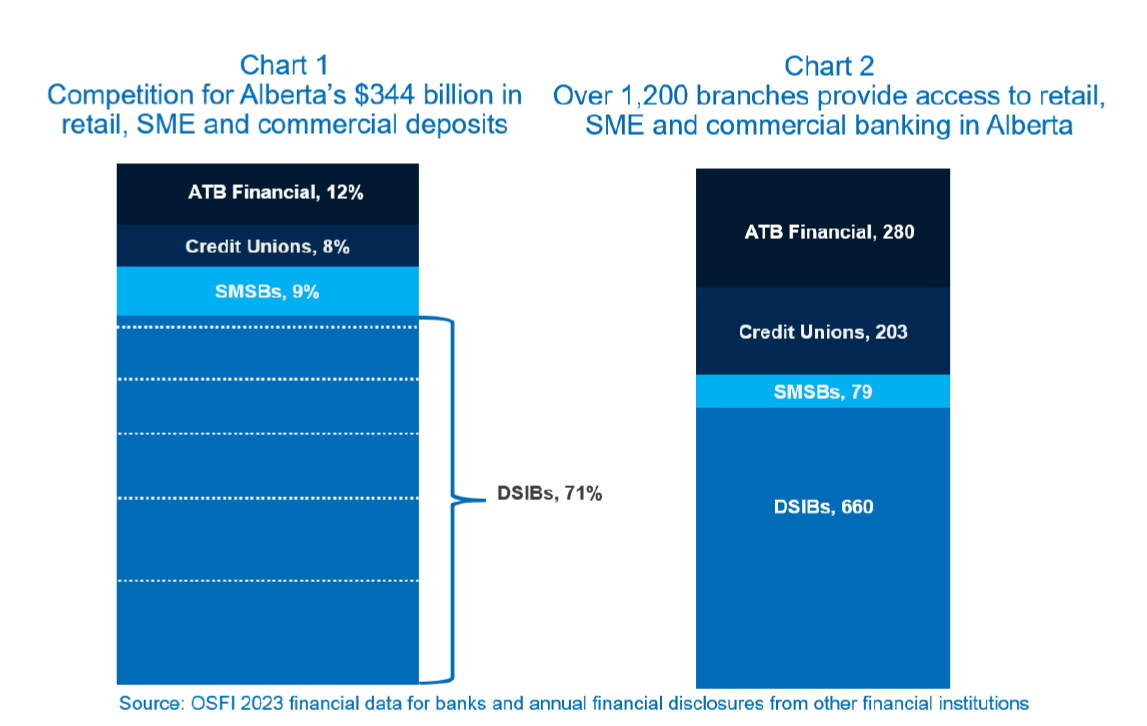

The financial services market is highly competitive in Alberta. For example, in Alberta’s market for retail, SME and commercial deposits, ATB Financial, 13 credit unions and over 30 small- and medium-sized banks (SMSB) accounting for nearly 30% of deposits with the six domestic systemically important banks (DSIBs) holding the remainder (Chart 1). Competition in the lending market is also high, with over 30 banks and federal credit unions able to underwrite insured mortgages to Albertans, competing with over 50 non-bank financial institutions such as provincial credit unions, mortgage finance companies, trust companies, insurance companies, and ATB Financial.3 Competition in the market for uninsured mortgages is particularly high due to mortgage investment companies and private lenders operating in the mortgage market.

Furthermore, while Canadians increasingly prefer digital banking,4 deposit taking institutions have a dedicated network of over 1,200 branches in Alberta to provide a local presence and access to in-person banking services (Chart 2). In total, bank branches account for around 60% of all deposit-taking institution branches in the province.

This competition is even more intense when the market is examined from the perspective of all financial services offered to Albertans. Market competitors include other deposit-taking institutions, life and health insurance companies, general insurance companies, trust companies, mutual funds, securities dealers, investment advisers and specialized finance companies and non-traditional firms entering and expanding the market. This includes large technology platforms with growing access to consumer data and fintech payment services providers, buy-now-pay-later companies, digital currency exchanges, robo-advisors, etc.

Amidst the growing competition in the evolving financial marketplace, the top six Canadian banks have invested approximately $120 billion in technology over the past decade. These investments have contributed to making the banking sector among the most highly productive business sectors in the Canadian economy.

Furthermore, the banking sector has seen labour productivity growth of 2.4% a year since 2007, making the Finance and Insurance sector the second fastest growing in terms of labour productivity since 2007 in the Canadian economy.5

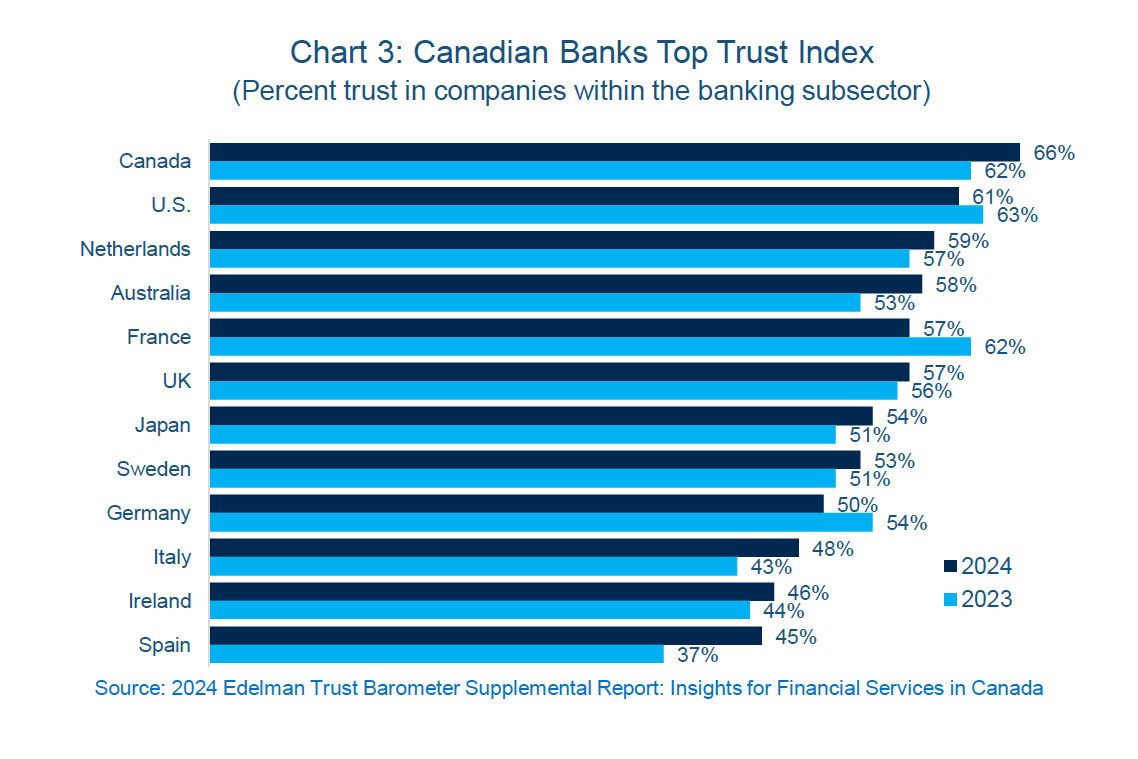

These investments also underpin Canadian banks’ commitment to further consumer trust and a reason why five of the world’s top 15 safest and most dependable commercial banks are Canadian.6 According to the 2024 Edelman Trust Barometer, Canadian banks have increased trust with the public over the past two years and Canadian banks are leading in trust with the public compared to banks in other developed countries (Chart 3).7

Recommendation 1

Scams are a growing threat, with scam losses reaching historic highs in the Canadian context. While 75% of Canadians report encountering a scam at least once a month, the Canadian Anti-Fraud Centre (CAFC) reported a staggering $569 million lost to scams by Canadians in 2023.8 However, as an estimated 90% of incidents are unreported, actual losses are believed to be significantly higher and may be as much as $11 billion annually (or 0.5% of Canada’s GDP).9 In Alberta alone, the CAFC has identified that nearly $40 million has been lost to fraud and scams between January to September of 2024 – note that this figure also only represents 5-10% of all scams reported.10

Protecting Canadians against scams is a shared responsibility that requires a coordinated, multi-sector strategy to effectively combat the evolving sophistication of scammers and mitigate rising consumer angst. A robust anti-scam strategy should:

- Educate Canadians on what they can do to reduce their exposure to scams and how to report them. Financial literacy is a core component of scam prevention and the broader well-being of Canadians.

- Prevent scams by creating the conditions to minimize opportunities for scammers to target Canadians.

- Respond effectively and with empathy to scam victims.

We must learn from the experience in other jurisdictions and take steps to proactively protect Canadians. Australia, for example, saw a significant increase in scams following the launch of real-time payments and consumer-driven banking. With the Real-Time Rail and consumer-driven banking on the horizon in Canada, Canada could see a significant increase in payments fraud. unless action is taken. These two initiatives, combined with the growing use of artificial intelligence, could see more sophisticated scams, and an increase in both number and amounts of financial losses. These risks underline the urgency to be proactive and mitigate potential harm to Canadians.

Canadians, governments, financial institutions, telecommunication companies, online platforms, technology companies, law enforcement, and the courts all have a significant role to play in this fight to reduce the occurrence of scams. Only by working together can we identify scammers more quickly and limit the damage they cause. We must focus on reducing the occurrence of scams by ensuring that scammers face consequences through the threat of capture and subsequent criminal prosecution. In order to do so, law enforcement requires sufficient resourcing and training across all areas of the judicial process (e.g., including courts, prosecutors) to be able to effectively prosecute identified scammers and deter future scam deployment.

Recommendation: We recommend that additional resourcing and specialized training be provided to law enforcement and the courts to be able to effectively address and stop the occurrence of scams that are being generated at an accelerated rate, to protect Albertans.

Recommendation 2

Federally regulated banks and their provincially regulated subsidiaries have long been entrusted with significant amounts of personal information, and protecting privacy continues to be paramount to maintaining customer trust. To protect the privacy of Albertans, the CBA strongly supports clear, nonconcurrent jurisdictional boundaries, to avoid potentially conflicting obligations and duplicative regulatory oversight. As a result, we support measures to harmonize federal and provincial rules to ensure a consistent approach to legislating privacy protection in the private sector. Alberta’s own reform efforts are currently in flight, with the Standing Committee on Resource Stewardship reviewing Alberta’s Personal Information Protection Act (PIPA) in the context of emerging trends in the digital and global marketplace while important ongoing efforts to reform PIPEDA have once again stalled and timing and nature of future reforms are uncertain.

Harmonization and interoperability can provide enormous benefits to Albertans by providing a familiar and common experience, regardless of residency or whether transacting with a bank or its subsidiaries. For Alberta businesses, harmonization facilitates cross-border operations, increases ease of compliance, enables organizations to provide more consistent products and services, and streamlines enforcement and consumer complaint regimes. These outcomes all drive increased consumer choice and access to innovative products and services, while effectively and efficiently protecting consumers’ privacy rights. Conversely, inconsistent privacy requirements for the private sector may lead to increased compliance costs and obstacles to innovation. For example, we note that a new Alberta public sector privacy bill introduces definitions that do not exist in today’s Canadian privacy context and may conflict with concepts used in the private sector, leading to confusion and increased regulatory red-tape if applied to private entities.

Harmonization will also be important to build trust in new federal initiatives that will also benefit Albertans. For example, the new federal initiative to combat financial crime through voluntary private-to-private information sharing is unlikely to protect Albertans or the Albertan economy if organizations perceive the sharing would not be supported under the province’s privacy laws, especially if fines or penalties are introduced without safe harbour protections. As another example, a future adoption of Consumer-Driven Banking in Canada would introduce a federal data mobility framework to securely exchange financial data. To ensure Albertans’ personal information is safe and secure, the province needs to ensure organizations would not be able to circumvent a federal framework with the introduction of any provincial data portability provisions that may conflict with federal rules.

Recommendations: Given the importance of interoperability and harmonization to consumers and businesses, we recommend the Government of Alberta continue to align its PIPA to the principles-based approach of federal privacy legislation as it will facilitate a consistent approach to private sector privacy domestically and globally for Alberta businesses and Albertans will benefit from a consistent approach to understanding their rights in relation to their personal information. We also recommend any new or amended definitions in PIPA be harmonized with existing private sector definitions and concepts, as inconsistent privacy requirements for the private sector may lead to increased compliance costs and obstacles to innovation. Lastly, any reform efforts should support pending or future federal initiatives aimed at increasing protections (e.g., combatting financial crime) or encouraging innovation (e.g., Consumer-Driven Banking).

Recommendation 3

It is critical that the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) continues to comprehensively govern the fight against money laundering (ML) and terrorist financing (TF) across Canada. While the CBA acknowledges that the PCMLTFA needs to continue its evolution into a risk-based framework that is fit for the purpose of combatting ML and TF, we caution against applying new provincial requirements, reporting or otherwise, to this space. We are concerned that any fragmentation of the national regime could inadvertently:

- Empower bad actors by creating opportunities for legislative arbitrage in Canada if regional or provincial requirements are misaligned with those at the federal level;

- Impact the ongoing, important national policy work of the federal government;

- Create coordination concerns amongst a growing number of authorities; and

- Potentially exacerbate concerns with high-level, low impact reporting.

Instead of considering new requirements to a comprehensively regulated space, the CBA urges the Government of Alberta to support existing Anti-Money Laundering (AML)/Anti-Terrorist Financing (ATF) tools and invest in law enforcement to better fight ML and TF. More specifically, the Government of Alberta should:

- Continue to support the federal government’s efforts to evolve the federal beneficial ownership registry into a single, pan-jurisdictional Canadian registry that reflects federal, provincial and territorial beneficial ownership information, as well as beneficial ownership information from other legal ownership structures (e.g., partnerships, trusts, and associations) – creating a one-stop-shop for users;

- Invest in law enforcement to support its investigation and prosecution of ML and TF cases and coordinate that work with relevant federal authorities; and,

- In coordination with the federal government, seek to enhance and refine the provincial forfeiture regime (i.e., Alberta’s Civil Enforcement Act) to adapt to the evolution of predicate offences and ML and recover criminal property.

In relation to the third point, we suggest the Government of Alberta provide funding and resources devoted to prosecutors and the courts in municipalities and regions with high volumes of financial crime. The funds would be used to establish specialist investigative units that boast the tools and knowledge to pursue financial crime charges. These municipalities and regions may be identified via a data sharing agreement with the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC).

These investments are critical. Without risking the unintended consequences outlined earlier in this section, they will bolster the federal regime and help transform FINTRAC intelligence into prosecutions, helping to protect everyday Canadians and the integrity of the Canadian financial system. The CBA and its members are eager to work with the Government of Alberta on this issue and look forward to consulting on and supporting provincial efforts.

Recommendation: We urge the Government of Alberta to work closely with the federal government and authorities to combat ML and TF. In particular, we urge investments in Alberta’s enforcement and prosecution of ML and TF and harmonize its existing tools with the federal government. A harmonized approach will ensure efficiency by avoiding compliance duplication across different levels of government.

Recommendation 4

Albertans, along with all Canadians, continue to adopt new payment methods offered by non-traditional payment service providers (PSPs), including Big Tech. At present, these PSPs are largely un- or under-regulated.

Globally, the G20 and OECD have recognized that financial consumer protection requires a more targeted set of principles than general consumer protection. These principles seek to mitigate key risks to consumers in financial transactions including, but not limited to:

- Incurring fees that have not been properly disclosed by a provider;

- Not having access to funds held by a provider;

- Being held responsible for fraudulent transactions; and

- Not having a line of recourse in the absence of a clear complaints-handling process.

Failure to address these risks, among others, can decrease consumer trust in the financial system. Financial services and products have the potential to disproportionately impact the well-being of consumers and must be addressed specifically rather than through overarching consumer rights across banks and PSPs.

While the Bank of Canada and Finance Canada have developed a federal supervisory framework for PSPs under the Retail Payment Activities Act to address certain financial and security risks, the framework is silent on market conduct. Addressing the market conduct gap is important to ensure PSPs provide fair consumer outcomes that encompass consumer protection. With some 3,000 PSPs currently operating in Canada and expected increases in consumer usage of PSPs once they are supervised by Bank of Canada, the absence of market conduct regulation is a significant gap in consumer protection.

It is important that Alberta work to align its market conduct approach with other provinces and the federal government to provide an overall consistent framework in Canada. This would ensure similar protections for consumers across the country as well as avoiding duplication or differing rules for Alberta-based PSPs that operate in multiple provinces.

We believe that Albertans and Canadians should continue to benefit from secure, reliable and consistent financial services. Therefore, it is important that un- or under regulated players do not introduce risk into the existing stable financial system. Ultimately, any market conduct framework would abide by the principle of “same activity, same risk, same regulation.”

Recommendation: We encourage the Government of Alberta to support the adoption of a financial consumer protection regime targeted at PSPs, as part of Alberta’s consumer protection framework. Enhancing standards for financial consumer protection should also extend to entities that embed payments processing for merchants on behalf of consumers that have the potential to fall outside the federal framework, as they introduce the same risks as PSPs. We also encourage Alberta to work with other provinces and the federal government to achieve a consistent market conduct framework across the country for the benefit of consumers and PSPs.

Recommendation 5

Banks are regulated federally; however, Alberta directly regulates another component of the deposit-taking marketplace – provincial credit unions. Alberta presently has 13 credit unions holding over $34 billion in assets and over $28 billion of deposits – amounting to 8% of total retail, SME and commercial deposits in the province.

As the regulator of the credit union sector, the Government of Alberta must meet the dual challenge of managing risk to the province while letting credit unions with growth aspirations scale up and expand to grow and compete. The federal credit union charter was created to address this challenge – it provides an avenue for credit unions to develop to grow and diversify beyond their own province, which reduces risk to the provincial government. Given the human, technological, and financial resources needed to compete in the financial services market, expansion under the federal framework allows federal credit unions to benefit from economies of scale and scope, increase consumer and business coverage to better manage risk through geographical diversification, and attract and retain employees with specialized skills to better compete with both traditional existing and emerging competitors.

There are several steps that can be taken to help facilitate provincially regulated credit unions to transition to the federal credit union charter. The government should work with credit unions to ensure their Board of Directors’ and members’ choice for the optimal business structure is supported by:

- Regulation to ensure a smooth and efficient process for provincial credit unions to transition to the federal level as stand-alone or amalgamated entities and ensuring requirements (including approvals) be proportionate to the transaction.

- Amending the Alberta Credit Union Act to make it easier for provincial credit union assets to be acquired by a federal credit union.

One of the benefits of the federal regulatory framework for financial institutions is that it provides an exceptional degree of transparency. Federally regulated credit unions and banks are required to provide quarterly and monthly financial disclosures that are published on the OSFI website.11Such transparency will increase the understanding of key risks, promote confidence, and stability in Alberta’s financial system. The CBA recommends that the Government of Alberta collect and publish similar financial information for provincially regulated credit unions. While most credit unions annually disclose their financial reports on their respective sites, more frequent and consistent disclosures on a centralized portal will improve the transparency of the credit union system’s financial state, which will help inform depositors and borrowers when making personal financial decisions.

Lastly, to ensure Canada’s financial system continues to remain one of the safest and reputable in the world, Alberta’s unlimited deposit guarantee should be reexamined to align with both international and national best practices.

Recommendation: We urge the Government of Alberta to provide policy and regulatory support to facilitate framework for those provincially regulated credit unions that want to transition to the federal credit union, increasing transparency in the provincial credit union system, and realigning credit unions’ unlimited deposit guarantees to international and national best practices.

Recommendation 6

Alberta has made encouraging efforts to address public safety concerns through a coordinated response between the province, city, and local partners. However, escalating crime and violence is affecting communities across Alberta in unprecedented ways. Increasing crime rates result in injuries, employees in fear of going to workplaces, businesses forced to close, loss of family-supporting jobs, and increased pressures on mental health support programs. Increasing resources for individuals with mental health concerns, economic stressors, or permanent housing would aid in alleviating the affects to the areas of concern.

Banks are committed to doing their part to support local communities. Thereby, we recommend the province work to expand the adoption of digital payments options for social benefits recipients and move away from physical cheques. This would not only deliver significant efficiency to the delivery model, but it would also further reduce risks to recipients while improving safety and security for branch staff.

The CBA is continuing its work as a member of the Downtown Recovery Coalition (DRC), a group of for- and not-for-profit business and community leaders committed to revitalize the Edmonton downtown area. The DRC recovery efforts focus on three pillars: safety and security, cleanliness and infrastructure, and transformational projects. However, the safety challenges CBA members are experiencing are not limited to Edmonton, the challenges have expanded to many rural and urban centers across the province, with branch employees being the first line of defense to many of these challenges.

The CBA also wants to highlight the importance of meaningful and appropriate response to incidents involving individuals experiencing mental health challenges or addiction related crisis. Other jurisdictions have developed programs where Mobile Crisis Units, of crisis workers and specially trained police officers, are used to de-escalate such interactions and provide onsite and future community program support to the individuals as appropriate. We encourage the Government of Alberta to explore deploying such crisis response units in the province.

Recommendations: We recommend implementing innovative, aggressive, and comprehensive solutions to address public safety and security challenges that impact community vitality and economic growth. Urgent and additional funding is required to enhance community vibrancy projects, expand pre-and post-addiction recovery services and support enhanced mobile crises response units. Additional efforts should be made to expand the adoption of digital payment options for all social benefits recipients.

Recommendation 7

Canada’s labour productivity growth has diminished considerably, making production more expensive and Canada less competitive. This diminished growth impacts Canada’s living standards, ability to pay for government programs, and economic resiliency. In fact, Canada ranks 18th in productivity among countries in the OECD and last among the G7.12 The CBA agrees with Premier Danielle Smith’s remarks that all levels of government need to pull in the same direction as there are too many regulatory roadblocks, too much red tape, too many interprovincial barriers, and too many taxes.13

Furthermore, the IMF, OECD, and others have urged Canada to implement growth-oriented tax policies to reverse Canada’s poor productivity trend. Yet, the federal government has imposed specific taxes on the banking sector, limiting its economic contributions. For banks, such taxes limit the amount of capital they can deploy to businesses for productivity enhancing measures, reducing Canadians’ ability to save and invest, increasing investment uncertainty, and reducing banks’ ability to attract necessary capital. Indeed, Australia’s Government Productivity Commission concluded that industry levies must be avoided to establish or maintain sound foundations for productivity growth.14

These taxes include:

- Recent removal of the Dividend Received Deduction, which will negatively impact middle-class Canadians who hold over 3 million retail market-linked GICs and Notes. These investments allow middle-class households, mostly approaching or in retirement, to access higher returns and manage downside risk.

- The Financial Institutions Tax and the Canada Recovery Dividend, announced in the 2022 Budget, which reduced the amount of capital that can be deployed to businesses and consumers as every dollar reduction in retained earnings translates into over $7.50 of foregone new credit capacity. These taxes have also deterred foreign investment into Canadian banks. In the year before the 2022 Budget, international investors made net purchases of $3.6 billion worth of Canadian bank equity. In the year afterwards, international investors made net divestments of $11.6 billion in Canadian bank equity.

The federal government has implemented retroactive sales taxes on payment clearing services. Retroactive taxes undermine the principles of predictability, certainty, fairness and confidence in the tax system needed by businesses to make investment decisions.

Comprehensive tax reform, including removal of sector-specific taxes, is needed to improve Canada’s productivity, living standard, competitiveness, and economic growth.

Recommendation: We recommend the Government of Alberta continue to undertake productivity-enhancing tax reforms in the province and advocate at the federal level for a comprehensive review of our country’s tax system. Canada must modernize its tax system and avoid asymmetrical, sector-specific taxes, and retroactive tax legislation that ultimately impacts consumers and undermines certainty around investment decisions.

Conclusion

The CBA thanks the Government of Alberta for the opportunity to contribute to its upcoming budget. Our recommendations address critical areas that impact families and businesses in Alberta and aim to ensure Canada’s banking system continues to support vibrant and healthy communities across the province.

We welcome further opportunities to discuss our recommendations in more detail and to explore collaborative efforts to positively impact the future of Albertans.

1 Banking contributions provided by CBA.

2 ISED, Credit Conditions Survey, 2010 to 2022.

3 CMHC National Housing Act Approved Lenders.

4 CBA, 2024

5 CBA calculations and Bennet Jones, Economic Outlook 2025, Safeguarding a Vital Relationship and Investing in a More Productive Economy. While the Finance and Insurance produced $93 in real GDP per hour worked, banking and other depository credit intermediation produced $113.4 in real GDP per hour worked.

6 Global Finance, World’s Safest Banks 2024: Commercial Top 50.

7 Edelman Canada, 2024 Edelman Trust Barometer Supplemental Report: Insights for Financial Services in Canada, 2024.

8 Global Anti-Scam Alliance, The State of Scams in Canada, 2023.

9 Royal Canadian Mounted Police, Fraud Prevention Month 2024: Fighting fraud in the digital era, 2024.

10 Figures provided by CAFC for the period of Jan 1st, 2024, to September 30th, 2024. This accounts for 2,920 reports filed to CAFC, resulting in 2,164 victims and $39,326,204.89 in losses.

11 OSFI, Financial data for banks.

12 OECD Compendium of Productivity Indicators 2023.

13 Canada’s Productivity Summit, Fireside Chat with Alberta Premier Danielle Smith, October 16 2024.